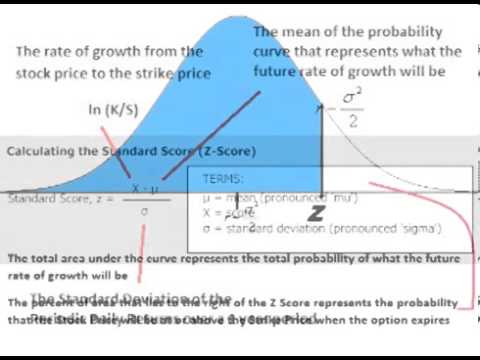

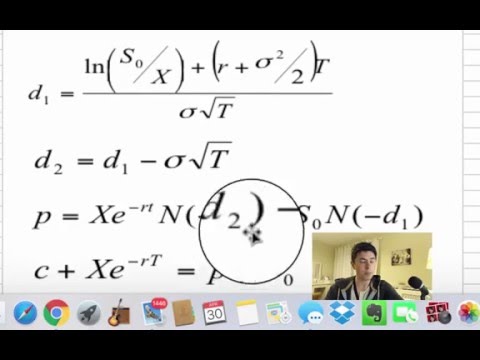

19. Black-Scholes Formula, Risk-neutral Valuation MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013View the complete course: http://ocw.mit.edu/18-S096F13Instructor: Vasily StrelaThis...

![]()

Copyright 1996-2024 Action News. A Division of WestNet Continental Broadcasting.

News Desk