Canadians watching the North American housing market are paying close attention to mortgage rate forecasts—and right now, experts say the picture remains remarkably uncertain.

Mortgage rates in the U.S. market, which heavily influence Canadian lending, have climbed sharply since the start of spring 2026. In early March, the average rate on 30-year mortgages sat at just 5.75%, according to Zillow data. By mid-April, that figure had jumped to 6.12%—a seemingly modest increase that translates to tens of thousands of dollars in additional interest costs over the life of a typical $400,000+ home loan.

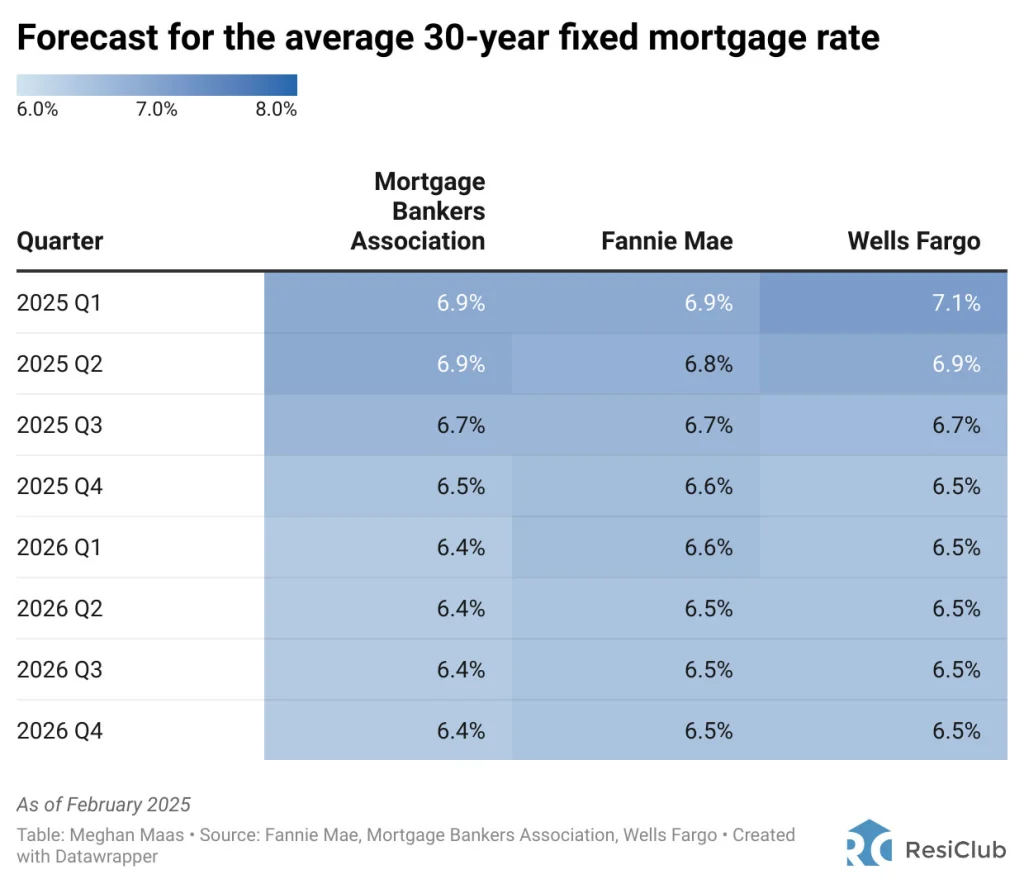

What Could the Rest of 2026 Bring?

Most industry experts believe mortgage rates will settle near the current 6% range by year's end. The Mortgage Bankers Association is forecasting an average rate of 6.2% on 30-year mortgages by December 2026—essentially where rates are trading today.

"Predictions are hard, given today's conditions," says Bill Dawley, senior vice president of residential lending at Amegy Bank. "But we expect rates to remain in the low 6% range through the end of the year."

Volatility Is the Real Story

The challenge for mortgage brokers and lenders right now isn't predicting the direction of rates—it's managing the whiplash of daily market swings.

"The mortgage trading desks hate not knowing which direction the wind is blowing," explains Kevin Leibowitz, mortgage broker at Grayton Mortgage. "When interest rates bounce around, the trading desks don't get aggressive in setting rates. That uncertainty keeps everyone cautious."

Nicole Rueth, senior vice president at The Rueth Team of Cross Country Mortgage, describes the current environment bluntly: "The range of outcomes is genuinely wide."

"What we've seen this year is a push-pull between fear and hope. Rising oil prices and inflation concerns push rates up. Then there's a headline about ceasefire talks or de-escalation and investors rally, yields drop, and rates pull back. We've had multiple swings in a matter of days. Borrowers quoted a rate on Monday get a different number by Thursday."

Geopolitics Are Driving Everything

The primary culprit behind rate volatility and recent increases? Geopolitical uncertainty. Oil price movements, inflation expectations, and their ripple effects through bond markets are creating an unusually turbulent environment for mortgage pricing.

"Geopolitics is driving everything right now in a way we haven't seen in a while," Rueth explains. "Oil prices feed into inflation expectations, inflation expectations feed into the 10-year Treasury yield, and the 10-year drives mortgage rates."

Two Possible Paths Forward

Experts see two competing scenarios for the rest of 2026:

The Optimistic Case: If geopolitical conflicts de-escalate, oil prices stabilize, and inflation remains under control, mortgage rates could drift back toward the low-to-mid 6% range—roughly where most forecasters expect them to settle anyway.

The Pessimistic Case: If global tensions escalate and oil prices continue climbing, mortgage rates could spike higher as inflation concerns resurface and bond yields rise accordingly.

"Right now, the market is trading on headlines more than data," Rueth says. "That kind of volatility tends to resolve in one direction eventually. We just don't know which one yet."

For Canadian homebuyers and homeowners considering refinancing, the takeaway is clear: expect continued rate uncertainty through 2026, and lock in any favourable rates as soon as they appear. The current environment rewards those who move quickly.

This article is based on reporting from CBS News, published April 15, 2026.