Mortgage rates are finally showing signs of sustained improvement after weeks of jarring swings that left would-be homebuyers scrambling for answers. As of April 24, 2026, the 30-year mortgage rate has dipped below the 6.20% threshold—a level that seemed unreachable just a few weeks ago when trade-driven market turbulence was pushing costs higher daily.

The encouraging shift comes as Treasury yields cool and trade tensions show early signs of easing. For sidelined buyers waiting for breathing room, this moment could represent a meaningful window of opportunity—but experts warn the opening may not stay ajar for long.

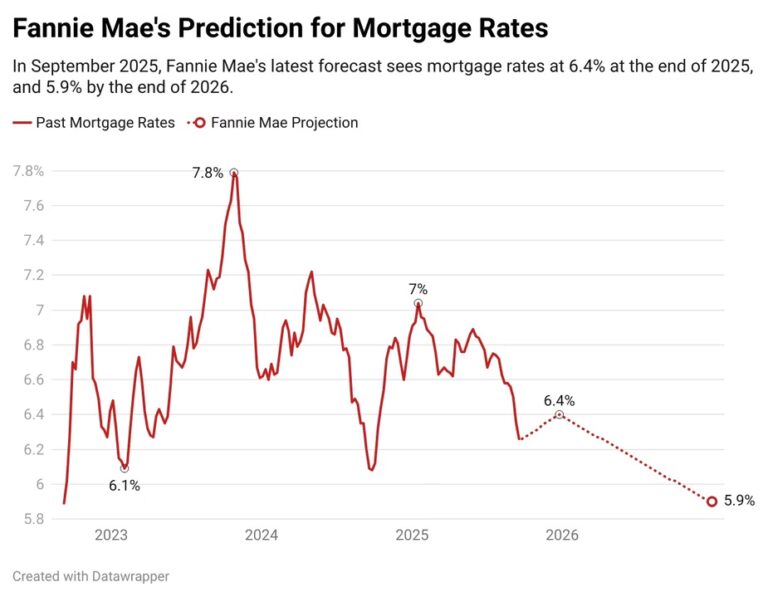

Where Rates Stand Today

The average 30-year mortgage rate currently sits at 6.13%, while the 15-year mortgage rate averages 5.63%—both marking notable improvements from earlier this month. The half-percentage-point gap between the two terms is significant: borrowers with the financial capacity to handle higher monthly payments on a 15-year loan could save tens of thousands in total interest over the life of the loan.

On the refinance side, homeowners considering a reset will find the 30-year refinance rate averaging 6.53%, with 15-year refinances at 5.64%. For those who locked in rates at 7% or higher, today's environment represents one of the more compelling refinancing opportunities in recent months.

Is Now the Time to Act?

The Federal Reserve has signalled it remains in no rush to cut rates, and ongoing uncertainty around trade policy means market conditions could shift quickly. Financial experts advise buyers and refinancers not to delay decision-making.

"The window that appears to be opening right now may not stay open long," analysts note, pointing to the unpredictable nature of bond markets in an uncertain trade environment.

For those considering refinancing, calculating your break-even point is essential—the number of months required for monthly savings to offset closing costs. If you plan to remain in your home well beyond that threshold, refinancing at today's rates could deliver significant long-term savings.

What Affects Your Rate

Keep in mind that these are averages. Your actual mortgage offer will depend on multiple factors, including credit score, down payment size, and debt-to-income ratio. Comparing quotes from several lenders before committing is one of the most effective ways to ensure you're not overpaying.

Data sourced from current market analysis as of April 24, 2026. Rates subject to change based on market conditions and lender policies.